Many young adults leave school knowing how to solve equations, write essays, and pass exams. Then the first paycheck arrives, and suddenly the questions become very different. Why is take-home pay lower than expected? How do credit cards actually work? What is a good credit score? And why does everyone keep talking about investing early?

Financial literacy has become one of the most valuable life skills, yet many people learn it through trial and error. Rising living costs, student debt, subscription spending, and constant financial advice on social media make it even harder to separate useful information from noise. The good news is that a few core concepts can create a much stronger financial foundation than most people realize.

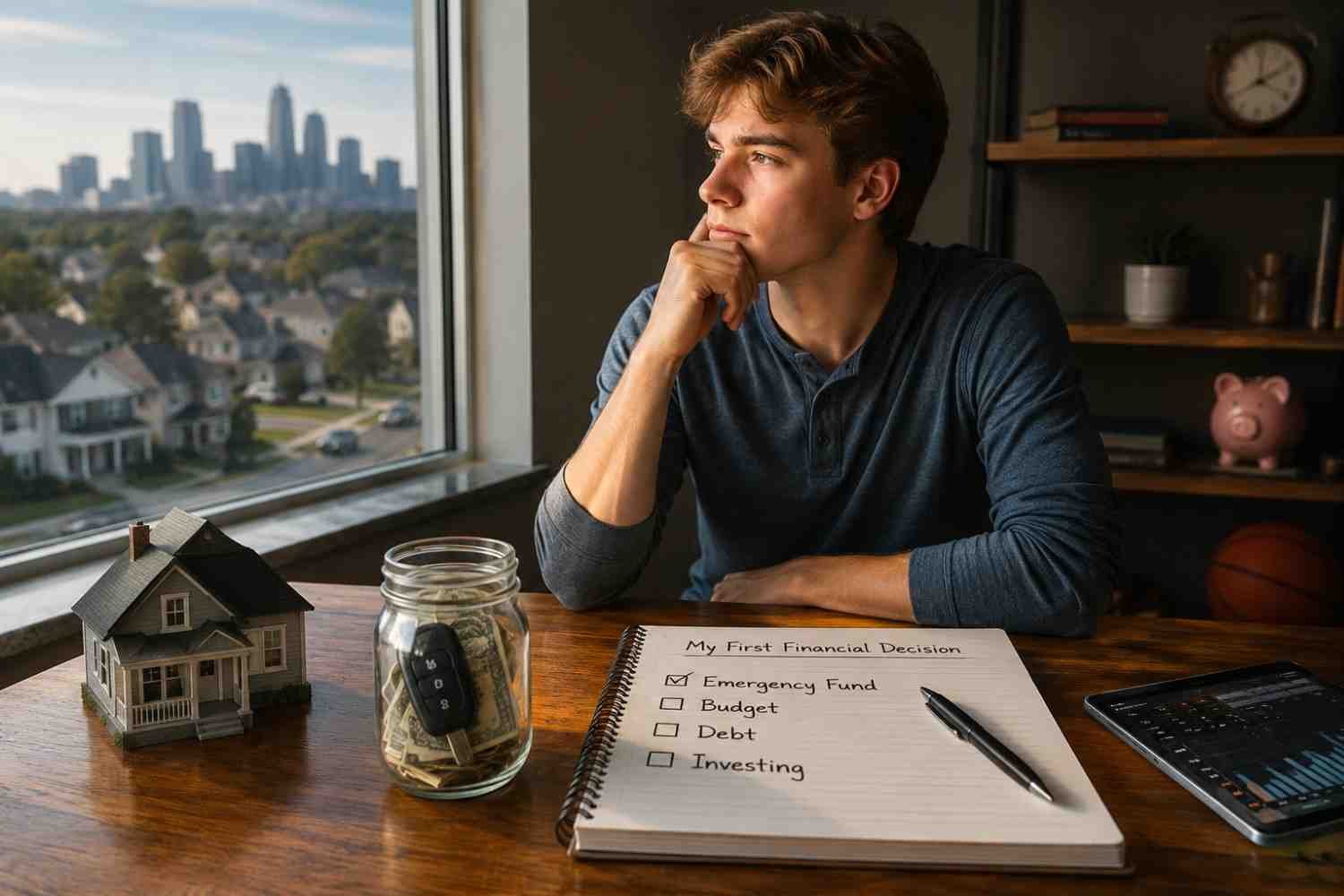

Your First Financial Decision Isn’t Investing

When people think about money, they often jump straight to investing. In reality, the first step is understanding cash flow.

Simply knowing where your money goes each month can prevent many financial problems. A budget does not need to be complicated. It only needs to provide clarity. One popular framework is the 50/30/20 rule, which allocates roughly 50% of income toward needs, 30% toward wants, and 20% toward savings or debt repayment.

What makes budgeting effective is not restriction. It is awareness. Many young adults are surprised to discover how much small recurring expenses, food delivery orders, and unused subscriptions affect their monthly finances.

Understanding the difference between wants and needs becomes especially important when income starts increasing. Without that awareness, higher earnings often lead to higher spending rather than greater financial security.

The Difference Between Having Credit and Managing Credit

Credit plays a larger role in everyday life than many people realize.

A credit score can influence apartment applications, vehicle financing, insurance rates, and future borrowing opportunities. Yet many young adults do not understand how scores are calculated until they need one.

Payment history remains one of the biggest factors. Consistently paying bills on time helps establish a positive credit profile. Credit utilization also matters. Using a large percentage of available credit can negatively affect scores, even when payments are made on time.

Credit cards themselves are not inherently good or bad. When used responsibly and paid in full each month, they can provide fraud protection, rewards, and credit-building opportunities. Problems often begin when balances carry over month after month, allowing compound interest to work against the cardholder rather than for them.

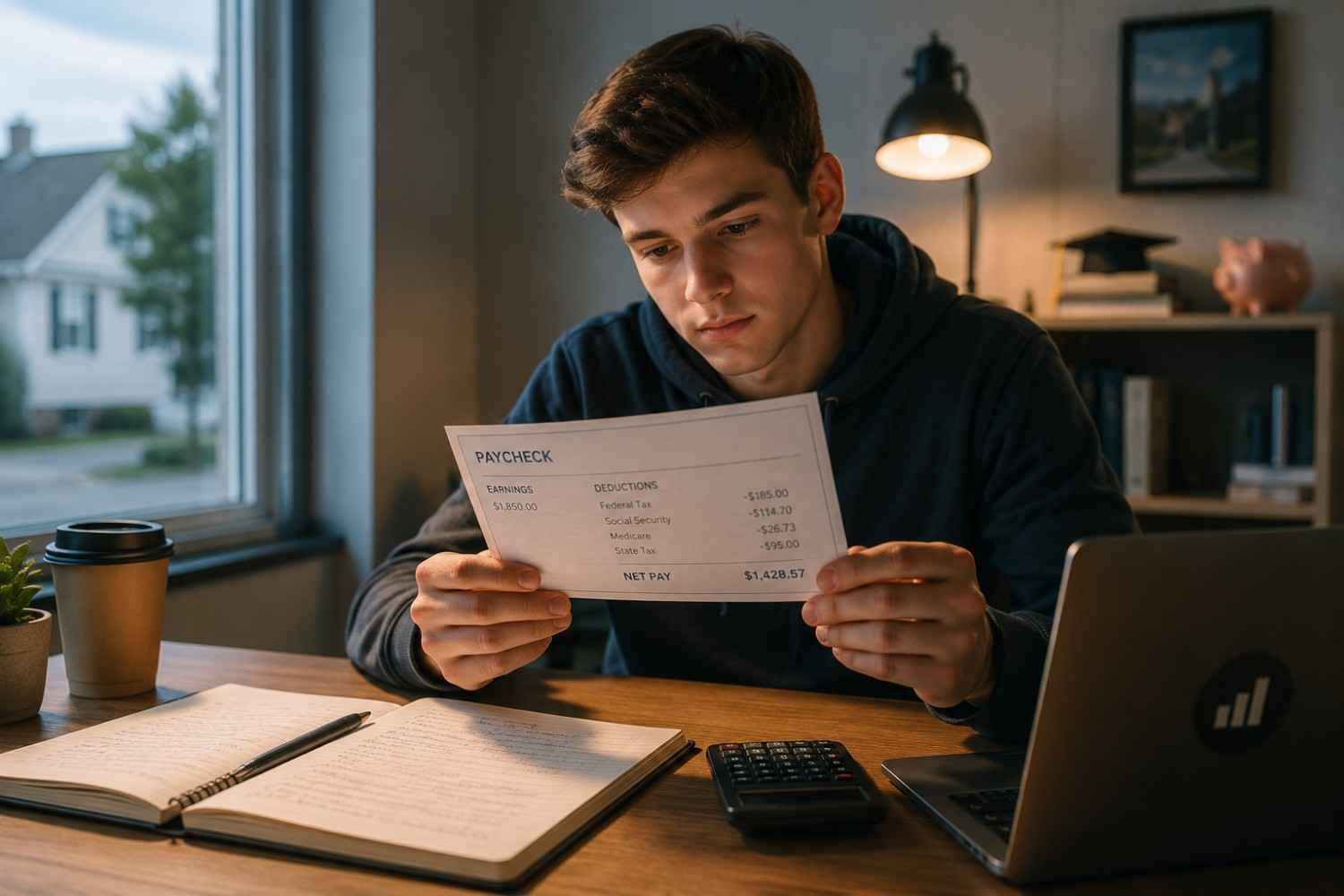

Why Understanding a Paycheck Matters?

The first full-time job often introduces a surprise: gross income and take-home pay are not the same thing.

Gross income represents total earnings before deductions. Net income is what actually arrives in a bank account after taxes and other withholdings. Understanding this difference helps young adults create realistic budgets and avoid overspending.

Basic tax knowledge is equally valuable. Knowing how tax brackets work, understanding common tax forms such as W-2s and 1099s, and becoming familiar with available filing resources can reduce confusion during tax season.

Many people assume financial success depends entirely on earning more money. In practice, understanding how income flows through taxes, deductions, and expenses is just as important.

The Financial Advantage of Starting Early

One of the most overlooked financial concepts is time.

Compound interest rewards people who start early, even when they begin with small amounts. A modest monthly contribution in your twenties often has more long-term impact than larger contributions started decades later.

The principle behind compound growth is simple: earnings generate additional earnings over time. As years pass, growth begins to accelerate.

These are often the most important wealth-building lessons from everyday life because they show that consistency frequently matters more than perfection. Financial progress is rarely created by a single great decision. It is usually the result of many small decisions repeated over the years.

This mindset also removes pressure. Young adults do not need large investment accounts to benefit from compound growth. They simply need to start.

Retirement Planning Is Not Just for Older Adults

Retirement can feel distant when someone is just beginning a career. However, the early years often provide the greatest opportunity to build long-term wealth.

If an employer offers a 401(k) match, contributing enough to receive the full match is often one of the smartest financial moves available. Many financial professionals describe employer matching contributions as part of total compensation because it effectively adds money to an employee’s retirement savings.

Individual Retirement Accounts, including Traditional and Roth IRAs, provide additional opportunities to save for the future. The right option depends on factors such as income, tax situation, and long-term goals.

The most important lesson is that retirement planning becomes easier when started early rather than delayed.

Protecting What You Build

Financial knowledge is not only about earning, saving, and investing. It is also about protecting assets.

Health insurance remains one of the most important financial safety nets available. Understanding deductibles, copays, and out-of-pocket maximums before a medical issue occurs can prevent costly surprises.

Renters insurance is another frequently overlooked tool. For a relatively low monthly cost, it can help protect personal belongings from theft, fire, and certain types of damage.

Digital security has become equally important. Financial accounts should use strong passwords and multi-factor authentication whenever possible. Credit freezes can also help prevent identity theft by restricting unauthorized credit applications.

Building wealth matters. Protecting it matters just as much.

FAQs: The Essential Financial Knowledge for Young Adults That Schools Rarely Teach

1. What financial skill should young adults learn first?

Budgeting and cash flow awareness are often the best starting points because they influence every other financial decision.

2. Why is a credit score important?

A credit score can affect borrowing costs, apartment approvals, insurance rates, and future financial opportunities.

3. When should someone start investing?

The earlier the better. Starting young gives compound interest more time to work and build long-term wealth.

4. Is saving enough, or should young adults invest too?

Savings provide short-term security, while investing supports long-term financial growth. Both play important roles in a healthy financial plan.

The Money Lessons That Tend to Matter Most Later

Many financial mistakes are not caused by a lack of intelligence. They happen because nobody explained how money works in everyday life. Credit, taxes, insurance, investing, and budgeting affect major life decisions, yet many people learn these lessons only after making expensive mistakes. Developing financial literacy early creates more options, less stress, and greater confidence when opportunities or challenges arise.

The goal is not to know everything about money. It is to understand enough to make better decisions consistently.